Repaying my mortgage early | Jinesh Vohra - Part 2

Our founder and CEO, Jinesh Vohra, recently had the pleasure of talking to Sam Abrika on the Nova Money Mindset podcast. He talks about his personal journey having paid off his mortgage and how his experience led him to build Sprive.

You can listen to the full podcast here and we’ve also made an edited down version of the interview available for you to read. Here is part 2 of the interview.

How easy is it to change your mortgage and make overpayments?

I think it varies from product to product and lender to lender. With some products being highly flexible and others being less so. A lot of the features around mortgages aren’t very transparent. For example, most lenders allow you to overpay 10% of your outstanding mortgage but they don’t typically promote that they allow you to do this and so you have to work things out for yourself.

Many lenders have two ways of processing overpayments. One is to keep your monthly payments the same and the other is to have the effect of reducing your monthly payments. Whilst lower monthly payments might seem like a good thing, but you actually end up paying more interest and aren’t actually paying off your mortgage faster.

With most lenders, you have to notify them if you want your overpayments to keep your monthly payments the same and actually have the effect of reducing your term. My wife actually made the mistake of making overpayments without telling our lender and it was only later on that I realised that I wasn’t saving as much interest as I should have.

What other mistakes do homeowners make when making overpayments?

Many homeowners are scared off by the concept of early repayment charges. No one wants to be charged for doing something that ultimately might help them be in a better financial position. Whilst limits are often quite large, some people are just mentally put off by that word. Often limits aren’t as transparent or as straight forward as you would like. People can be put off as they may have to read the small print in their mortgage offer document to understand exactly, what you can do and what you can't do.

Even with the exit penalties, people often feel like they can't leave because they're within their deal period. In reality, it might make sense for you to leave early. However, you have to crunch the numbers and that's obviously time consuming and not easy.

Why is making overpayments made to be so complicated?

Most lenders will have a mortgage overpayment calculator that will show you the benefit of making overpayments. However, unfortunately, they don’t make it necessarily straightforward to make the payments. There are very few banking apps that will show you the benefits of making overpayments, help you make them with a single tap, or show you how much sooner you’re on track to pay off your mortgage.

When I was paying off my mortgage, I didn't know how much interest I was saving. I didn't really know if I was on track to pay off my mortgage eight years earlier, nine years earlier, 10 years earlier. All I knew is that I'm doing something positive to help me achieve a goal and that if I kept doing it for long enough, that eventually my outstanding mortgage balance would reach zero.

From a lender's perspective, they're in the business of making money. The longer people have mortgages, the more money they make. Typically, lenders also front-load interest payments. So in the early years of your mortgage, you're paying mostly interest and it’s only later in life that you really start paying the majority of what you borrowed. What you typically find is that most people in the UK, wait until later in life when they are approaching retirement. They suddenly start to realise they need to start paying it off in large chunks. Lenders are completely okay with that because by then, they've earned most of the interest during the earlier years of their mortgage.

How should you make overpayments regularly?

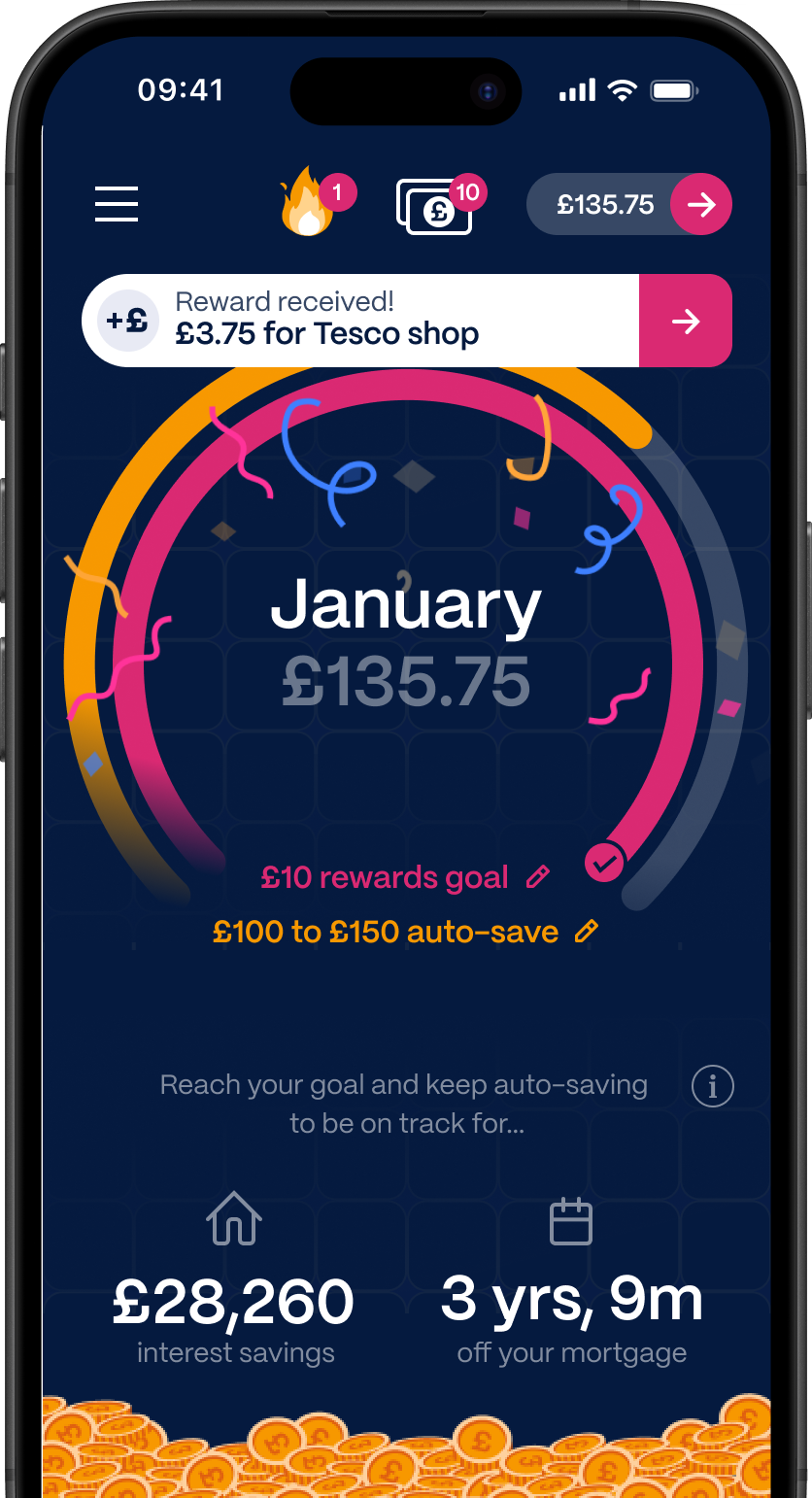

For many homeowners, their mortgage is their largest household commitment and will spend tens if not hundreds of thousands of pounds in interest over their lifetime. Why wait until late in life and let the lender essentially win. Putting your spare cash towards your mortgage will make a huge dent. You’ll be amazed at how much you can save, just by putting an extra £3 a day towards your mortgage. Our existing user base is on track to pay off their mortgage eight years earlier and save ~32,000 pounds in interest, on average, which is quite a sizable sum. So it just shows you, that if you're continually at it, it can make a huge dent, and have a huge impact on your finances.

What does a typical Sprive customer look like?

I would say they tend to be first time buyer who has been living in that property for at least or two and in a position where they are financially comfortable enough to meet their monthly payments. For them, they have discretionary income and it's for them to decide what they want to do that cash. Many of our customers don't like the idea of having a mortgage later in life, they want more control, they also realise that interest rates are low. So rather than keeping money in their bank account, where they're earning very little interest, they’re keen on doing something smart with their money. If you have money sitting in your savings account, not only do you earn very little interest on it, but you're likely to pay tax on it. It’s got many people thinking that with overpayments, I get the benefit of paying off my mortgage earlier, more control over my life, but I'm also saving more money too.

Some of our customers are very aggressive and they just want to get rid of it as quickly as they can. The majority of our customers, want to just chip away in a manner that doesn’t impact their lifestyle and gets them in a position where they don’t have a mortgage in their 70s.

How does Sprive help you make overpayments?

Our algorithm, helps you put money aside automatically so that with one tap you can payments to your lender. You link your bank account via open banking, so if in a given month you’ve spent a lot of money then a lot less money would be set aside versus a month where you’ve saved more than usual. You set the limit, so we will never impact your lifestyle more than you want us to.

Read more articles

Download Sprive today and start taking years off your mortgage

Sprive supports 14 of the largest lenders in the UK. It’s completely free.