Rebecca's Mortgage Story, an Interview with a Sprive Customer

To start, can you share what your mortgage journey has been like?

Rebecca:

Of course! We got our first mortgage when we were 26, and we’ve now had it for 9 years. Our journey began quite shakily because my husband had a poor credit score, which meant most high street banks wouldn't offer us a mortgage. Thankfully, a colleague recommended we use an independent mortgage broker. These brokers are usually free, taking their fee from the lender, and they have access to a vast range of lenders, which really helped us find better deals despite our circumstances. We ended up accepting a higher interest rate but were advised to take a two-year fixed deal. After those initial tough years, it became much easier to secure a better rate and fix it for five years.

That sounds challenging! How long did it take you to save for your mortgage?

Rebecca: I received an inheritance from my father when I was 19, which I saved diligently. My husband and I lived with my mum for about two years, saving every penny we could to buy our first home. We rarely went out, cooked all our meals at home, and shopped at the cheapest stores.

Every journey has its ups and downs. What would you consider your 'mortgage horror story'?

Rebecca: Ah, yes! The housing market was crazy at the time, and like many of our peers, we felt like we might never be able to buy. Once we had an offer accepted as first-time buyers, we were asked to jump through a lot of hoops and provide extensive documentation. We even had to sign undertakings agreeing to do significant work on the property, like treating damp and removing asbestos. Just when we thought we were in the clear, the lender asked for an extra £5,000. Fortunately, my husband’s family gifted him that amount, which helped equalize our equity. It was a very stressful time, especially since we had no savings left and a house needing renovations.

Did Sprive help you through these challenges?

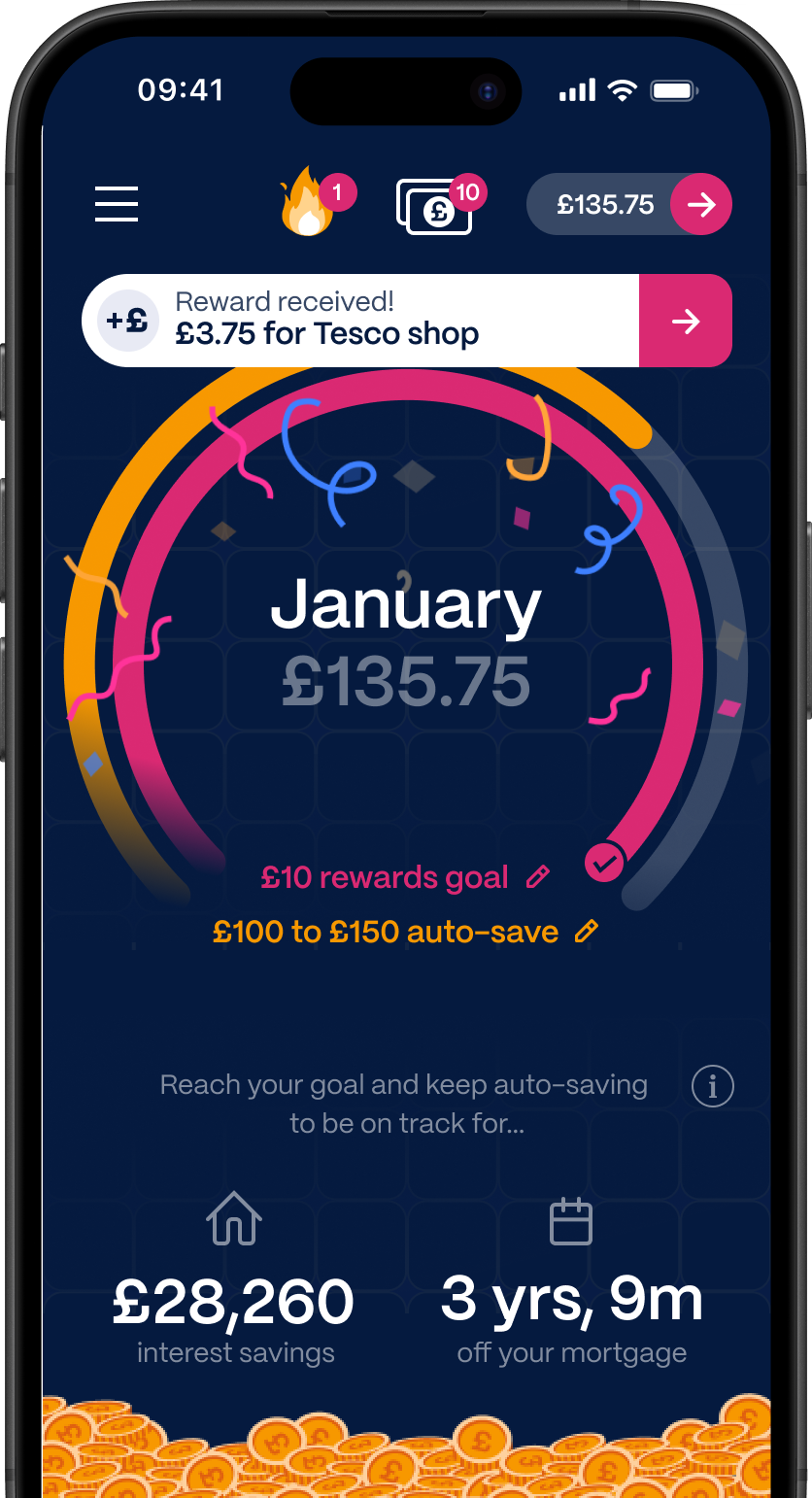

Rebecca: Now, nine years later, we’ve completed most of the necessary renovations, which have added value to our home. We decided to overpay on our mortgage, but with the cost of living crisis, we didn’t have much disposable income. That’s where Sprive came in. We set small monthly targets using the auto-save feature and regularly utilized cashback from gift cards and surveys. The app’s tracking function makes it easy to see how even small overpayments can save us a fortune in interest over the life of the mortgage.

What has been the most surprising thing you’ve learned since getting your mortgage?

Rebecca: Definitely how much interest you end up paying over time. You might think, “Oh, my house cost £200,000; that’s how much I’ll pay back,” but that’s not the case. With interest over such a long term, you’ll end up paying back many thousands more than the original amount borrowed.

How has having a mortgage changed your spending habits?

Rebecca: It’s made us much more mindful of our spending. We've had to prioritise our mortgage payments and debt reduction, which means saving for the future sometimes feels like a luxury we can’t afford right now.

Have you experienced any changes in your mortgage terms over time?

Rebecca: Yes, we did experience some term changes. Our first mortgage was for 30 years at a 4.7% interest rate, fixed for just two years. Fortunately, after that period, we were lucky that house prices increased, along with the renovations we completed. Our next deal was a 5-year deal for 18 years at 2.09%, which was a reduction of 10 years in term! Our latest deal, taken out in November 2022, is a 13-year term at 2.99%.

How do you balance saving for the future with making mortgage payments?

Rebecca: We’re fortunate to have good pension plans from our jobs, but aside from that, saving for the future can be tough. We focus on paying down debt and maintaining sinking funds for annual costs.

Do you stay informed about changes in mortgage rates or market conditions?

Rebecca: Initially, I had no real understanding of interest rates or the market. But over the past nine years, I’ve learned to pay attention to media coverage and have more productive discussions with friends and family about market conditions.

What’s your number one saving tip for others?

Rebecca: Get all the free money you can! Cashback, discounts, and deals add up over time. We embarked on a transformational debt-free journey in 2020 and changed our mindset about making money outside our 9-to-5 jobs. There’s a great community online that shares tips and tricks.

What does being a homeowner mean to you?

Rebecca: Having experienced housing insecurity in my childhood, it was crucial for me to have a safe and secure place to live—somewhere I wouldn’t be asked to leave unless it was my responsibility. While renting has its freedoms, I wanted to settle down and put down roots.

What is your number one financial goal?

Rebecca: To be totally debt-free, mortgage included.

Why are you using Sprive?

Rebecca: I love making small overpayments when big ones feel out of reach. Sprive gamifies the experience with a monthly tracker for how much we’ve overpaid and what percentage of our house we own. Plus, the cashback on purchases makes a big difference!

Read more articles

Download Sprive today and start taking years off your mortgage

Sprive supports 14 of the largest lenders in the UK. It’s completely free.