How to Remortgage Your Help to Buy Equity Loan

For many homeowners in the UK, the Help to Buy Scheme has been an important tool in helping them get onto the property ladder. More than 350,000 people used it to buy their first home, with more than £2.2 billion of support last year provided by the government.

However, once the initial loan period offered for five years ends, it’s important to consider remortgaging your loan to ensure that you’re getting the best deal possible and avoid an increase in your bills and unnecessary expenses like interest.

In this article, we’ll cover everything you need to know about how to remortgage your Help to Buy Equity Loan.👇

What is the Help to Buy Government Scheme?

The Help to Buy Scheme was launched by the UK government in 2013 as a way to help first-time buyers and home movers get onto the property ladder. The scheme provides a loan of up to 20% (40% in London) of the property’s value to put towards a deposit.

In this scheme, the government provides an equity loan of up to 20% of the property's value (40% in London) that is interest-free for the first five years. The buyer must contribute a deposit of at least 5% and obtain a mortgage for the remaining 75% (55% in London) of the purchase price.

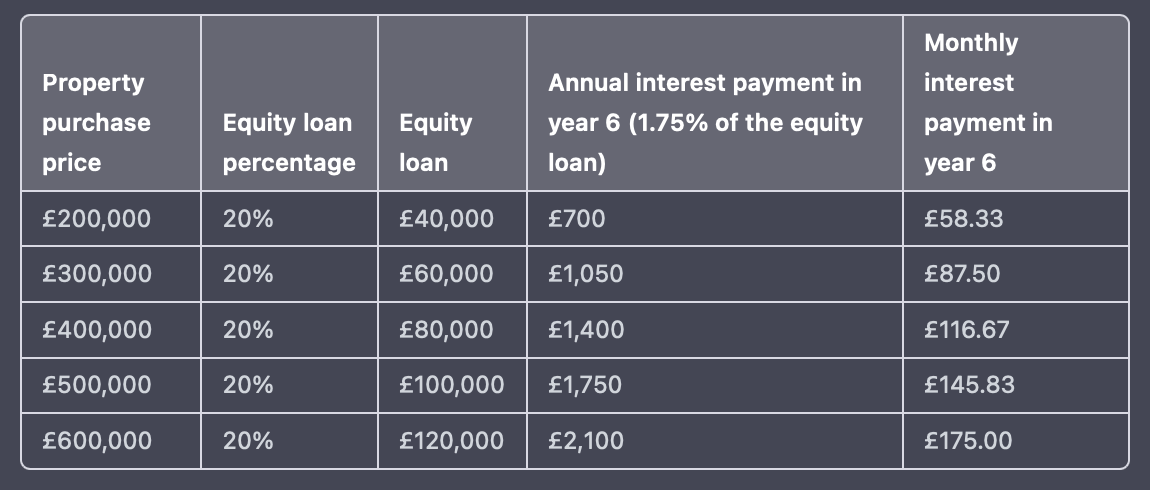

Let's say the property you want to purchase is worth £200,000. You would need to contribute a minimum deposit of £10,000 (5% of the property's value) and obtain a mortgage of £150,000 (75% of the property's value). The government would provide a loan of £40,000 (20% of the property's value) that is interest-free for the first five years.

This loan is interest-free for the first five years, after which interest is charged per annum. This must be repaid either when you sell your home or after a maximum period of 25 years.

What happens after the initial 5-year period?

After the initial 5-year period, you will need to start paying interest on the equity loan. The interest rate increases every year in April, by adding the Consumer Price Index (CPI) plus 2%. Read more here.

It is important to note that the amount of interest payable will depend on the value of the property at the time of repayment. If the value of the property has increased, then the amount of interest payable will be higher than if the property value had remained the same or decreased. Refer to the table below:

What are the options available to me?

At this point, you may choose to either pay off the equity loan in full or continue to pay the interest on the loan. Paying off the equity loan in full can be done through remortgaging, using savings, or selling the property.

If the property has increased in value, paying off the equity loan in full can be a smart financial move as it can result in significant savings in the long term.

However, it is important to note that if your house has sharply decreased in value, your options will be limited. Negative equity means that your home's resale value wouldn't be enough to repay the outstanding balance of your current mortgage.

If you choose to continue paying the interest on the equity loan, it is important to budget for the increasing costs especially in today's uncertain economic conditions. You can also consider remortgaging your property to reduce monthly payments and potentially save money on interest.

If you are approaching the end of your deal or 5 year interest free period, you may be unsure of the options available to you. Based on your personal circumstances, you should seek advice from a registered financial advisor or a Help to buy scheme administrator.

Can I remortgage Help to Buy Equity Loans?

Yes, you can remortgage your loan, but there are certain rules and regulations to follow. Firstly, you need to ensure that your current or new lender is happy to remortgage this. Not all lenders offer this service, so it's important to research and find a lender who can help you.

How can I remortgage my loan?

Before you start the remortgaging process, you need to know the current value of your property and the outstanding balance of your Help to Buy loan. You can get this information from your mortgage lender or the Help to Buy agent. Once you have this information, you can start shopping around for a new deal.

It's essential to compare different deals and lenders to find the best interest rates and terms that suit your financial circumstances. Once you have found the right deal, you can submit a full mortgage application to the lender. Read our article on remortgaging to find out more.

When applying for a remortgage, you will need to provide your lender with your income details, employment status, and credit score. Your lender will also need to know the value of your property and the remaining loan balance.

If you meet the lender's eligibility criteria, they will offer you a new deal that includes the repayment of your Help to Buy equity loan.

Do I need a solicitor?

It is recommended that you use a solicitor when remortgaging your Help to Buy loan. This is because the Help to Buy scheme involves a government equity loan that is secured against your property.

When remortgaging, you will need to pay off the loan with the new mortgage and make sure that the new mortgage complies with the rules of the Help to Buy scheme.

A solicitor can help you with the legal aspects of the remortgage process, including the transfer of the loan, ensuring that the new mortgage meets the requirements of the scheme. They can also handle any necessary paperwork and liaise with your mortgage broker and the scheme agency on your behalf.

What are the Benefits of Remortgaging my loan?

Remortgaging your Help to Buy equity loan can have several benefits, including:

Lower Monthly Payments:

One of the most significant benefits of remortgaging your Help to Buy equity loan is that it can reduce your monthly payments. By switching to a more competitive deal with a lower interest charges, you can save money on your monthly mortgage payments, which can be particularly helpful based on your financial goals and health.

Long-Term Savings:

Remortgaging your Help to Buy equity loan can save you money in the long term. By switching to a better deal with a lower interest rate, you can save thousands of pounds over the lifetime of your mortgage. This can help you to pay off your existing mortgage sooner and reduce your overall debt.

Greater Financial Flexibility:

Remortgaging your Help to Buy equity loan can give you greater financial flexibility. By choosing a deal that suits your budget and lifestyle, you can have more control over your finances. This can allow you to save money for other important expenses, such as home improvements, education, or retirement.

What are the potential challenges I may face?

There are several challenges or issues you may face when remortgaging your Help to Buy loan. Here are some of the most common ones:

Eligibility requirements

You must meet certain criteria such as having a good credit score, a stable income, and sufficient equity in your property. Failing to meet these requirements could result in you not being able to remortgage.

Suitable mortgage deal

Finding a mortgage deal that meets both your needs and the requirements can be a challenge. Some lenders may not offer Help to Buy remortgages or may have specific criteria that you must meet to qualify for the scheme.

Valuation issues

The value of your property can affect the amount you can borrow and the interest you are offered. If the value of your property has decreased, you may need to contribute more equity to meet the minimum loan-to-value requirements of the Help to Buy scheme. We recommend using a RICS certified surveyor.

Legal and administrative issues

The Help to Buy remortgage process can involve complex legal and administrative tasks, such as paying off the existing loan, transferring ownership of the equity loan, and registering the new mortgage with the Help to Buy agency. Failing to handle these tasks correctly can cause delays and complications.

Financial risks

Remortgaging carries financial risks, particularly if you are unable to make your mortgage payments. Non-payment could result in the loss of your property and equity loan, with serious financial consequences including repossession and negative impact on your credit score. It's essential to seek professional advice to ensure you understand the financial risks and consequences.

Conclusion

Remortgaging your Help to Buy equity loan can be a smart financial move for you. However, it's important to remember that not all mortgage lenders offer this service, and you need to meet certain eligibility criteria to be able to remortgage.

By comparing different deals and lenders, seeking advice from a registered financial advisor or a Help to buy scheme administrator, and using a solicitor during the remortgage process, you can potentially save money on interest and secure the best deal for your financial circumstances.